Not known Details About Mortgage Investment Corporation

Not known Incorrect Statements About Mortgage Investment Corporation

Table of ContentsThe Buzz on Mortgage Investment CorporationThe 6-Minute Rule for Mortgage Investment CorporationAll About Mortgage Investment CorporationExamine This Report on Mortgage Investment CorporationThe Mortgage Investment Corporation Diaries9 Easy Facts About Mortgage Investment Corporation Shown

After the lending institution sells the financing to a home mortgage investor, the loan provider can utilize the funds it gets to make even more finances. Besides giving the funds for loan providers to develop even more finances, investors are essential since they establish guidelines that contribute in what kinds of financings you can get.

Capitalists additionally manage them in different ways. Rather, they're marketed straight from lending institutions to exclusive capitalists, without entailing a government-sponsored enterprise.

These companies will certainly package the loans and market them to private investors on the secondary market. After you close the financing, your lender may offer your loan to an investor, yet this usually doesn't transform anything for you. You would still pay to the loan provider, or to the home loan servicer that manages your home mortgage payments.

The 10-Minute Rule for Mortgage Investment Corporation

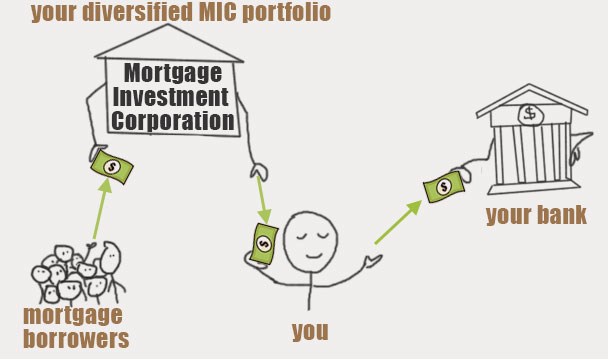

Just How MICs Resource and Adjudicate Loans and What Happens When There Is a Default Mortgage Investment Corporations offer investors with direct exposure to the genuine estate market via a pool of very carefully picked mortgages. A MIC is responsible for all elements of the mortgage investing process, from origination to adjudication, including daily management.

CMI MIC Finances' strenuous qualification process allows us to take care of home loan top quality at the really start of the investment process, reducing the possibility for settlement issues within the loan profile over the term of each mortgage. Still, returned and late repayments can not be proactively taken care of 100 percent of the time.

We buy mortgage markets across the country, enabling us to offer throughout Canada. For more information regarding our financial investment process, get in touch with us today. Contact us by completing the form listed below to learn more about our MIC funds.

The Greatest Guide To Mortgage Investment Corporation

A MIC is additionally considered a flow-through investment vehicle, which means it should pass 100% of its yearly net earnings to the investors. The dividends are paid to investors consistently, typically each month or quarter. The Earnings Tax Act (Section 130.1) details the demands that a company have to fulfill to qualify as a MIC: A minimum of 20 shareholdersA minimum of 50% of properties are property home mortgages and/or cash money deposits insured by the Canada Deposit Insurance Policy Firm (CDIC)Less than 25% of capital for each shareholderMaximum 25% of capital invested right into genuine estateCannot be associated with constructionDistributions submitted under T5 tax obligation formsOnly Canadian home loans are eligible100% of net revenue mosts likely to shareholdersAnnual monetary statements examined by an independent audit firm The Home mortgage Financial investment Company (MIC) is a customized monetary entity that spends largely in home loan.

At Amur Resources, we intend to supply a truly diversified strategy to different financial investments that maximize return and funding conservation. By using a range of conventional, revenue, and high-yield funds, we accommodate a variety of spending purposes and choices that fit the requirements of every individual capitalist. By purchasing and holding shares in the MIC, shareholders gain a symmetrical ownership interest in the business and obtain earnings through returns payouts.

Additionally, 100% of the capitalist's funding gets positioned in the chosen MIC without in advance deal costs or trailer fees. Amur Funding is concentrated on you could check here giving financiers at any level this contact form with access to properly handled personal mutual fund. Investment in our fund offerings is available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan citizens and should be made on a private positioning basis.

Purchasing MICs is an excellent way to get exposure to Canada's thriving realty market without the needs of active residential or commercial property management. Apart from this, there are several various other reasons that capitalists think about MICs in Canada: For those looking for returns comparable to the securities market without the linked volatility, MICs supply a protected property investment that's less complex and may be a lot more successful.

Mortgage Investment Corporation Fundamentals Explained

Our MIC funds have traditionally supplied 6%-14% yearly returns - Mortgage Investment Corporation. * MIC investors obtain rewards from the passion settlements made by borrowers to the home mortgage loan provider, forming a constant passive earnings stream at higher rates than conventional fixed-income protections like federal government bonds and GICs. They can likewise choose to reinvest the rewards right into the fund for worsened returns

MICs presently make up about 1% of the total Canadian mortgage market and stand for a growing sector of non-bank financial business. As capitalist need for MICs expands, it is very important to understand how they function and what makes them different from typical realty financial investments. MICs spend in home loans, unreal estate, and as a result supply direct exposure to the housing market without the added threat of residential or commercial property possession or title transfer.

generally between 6 and 24 months). Mortgage Investment Corporation. In return, the MIC gathers passion and charges from the borrowers, which are then distributed to the fund's liked shareholders as reward settlements, usually on a regular monthly basis. More hints Due to the fact that MICs are not bound by numerous of the same stringent loaning demands as standard financial institutions, they can set their very own standards for authorizing fundings

Mortgage Investment Corporation Can Be Fun For Everyone

Home loan Financial investment Firms additionally enjoy special tax obligation treatment under the Revenue Tax Obligation Act as a "flow-through" financial investment car. To avoid paying income tax obligations, a MIC has to distribute 100% of its net revenue to investors.

Case in factor: The S&P 500's REIT classification vastly underperformed the more comprehensive stock market over the previous 5 years. The iShares united state Realty exchange-traded fund is up much less than 7% considering that 2018. Comparative, CMI MIC Finances have traditionally generated anywhere from 6% to 11% yearly returns, relying on the fund.

In the years where bond returns continuously decreased, Home loan Investment Firms and other different assets expanded in appeal. Yields have actually recoiled given that 2021 as reserve banks have actually increased rates of interest however genuine returns stay adverse family member to inflation. Comparative, the CMI MIC Balanced Home loan Fund produced a net annual return of 8.57% in 2022, like its performance in 2021 (8.39%) and 2020 (8.43%).

How Mortgage Investment Corporation can Save You Time, Stress, and Money.

That is why we wish to aid you make an educated choice concerning whether or not. There are many advantages connected with buying MICs, including: Because financiers' money is pooled with each other and spent throughout multiple homes, their profiles are diversified throughout various real estate types and debtors. By owning a profile of home loans, financiers can minimize risk and prevent putting all their eggs in one basket.